Date Published: 18 December 2018

Authors: Bill Jamieson and Ken Chia.

Introduction

On 19 November 2018, following two rounds of public consultation over the past 3 years, the Monetary Authority of Singapore (“MAS”) finalised its new regulatory framework for payment services under the Payment Services Bill (the “Bill”), which was read in Parliament for the first time. The Bill streamlines the payment services regulatory framework under a single piece of legislation, meaning that the Payment Systems (Oversight) Act (Cap. 222A) (“PS(O)A”) and the Money-Changing and Remittance Businesses Act (Cap. 187) (“MCRBA”) will both be repealed at the commencement of the new law.

The Bill provides a necessary update to the regulatory framework of payment services in Singapore, in light of the recent proliferation of new and varied payment business models, such as Grab Holdings’ Grabpay, PayNow, cryptocurrency wallets and cryptocurrency exchanges, each accompanied with risks which may not be adequately regulated under the PS(O)A and MCRBA.

Scope of regulation

Under the Bill, MAS has introduced two parallel regulatory frameworks, namely:

- a designation regime that enables MAS to regulate operators, settlement institutions and participants of systemically important payment systems, such as interbank services, as “designated payment systems” for financial stability and efficiency; and

- a licensing regime that enables MAS to regulate providers of retail payment services to customers and merchants.

Designation and regulation of payment systems

MAS may designate a payment system as a designated payment system if it is satisfied that:

- a disruption in the operations of the payment system could trigger, cause or transmit further disruption to participants of the payment systems or the financial system of Singapore, or affect public confidence in the payment systems or the financial system of Singapore;

- the payment system is widely used in Singapore or may have an impact on the operations of other payment systems in Singapore and such designation is necessary to ensure efficiency or competitiveness in the services provided by the operator of the payment system; or

- the designation is in the interests of the public.

Under the Bill, MAS may impose conditions or restrictions as it thinks fit in relation to the activities undertaken by or the standards to be maintained by the operator or settlement institution of a designated payment system, or require such operator or settlement institution to operate as a corporation.

Licensing of retail payment service providers

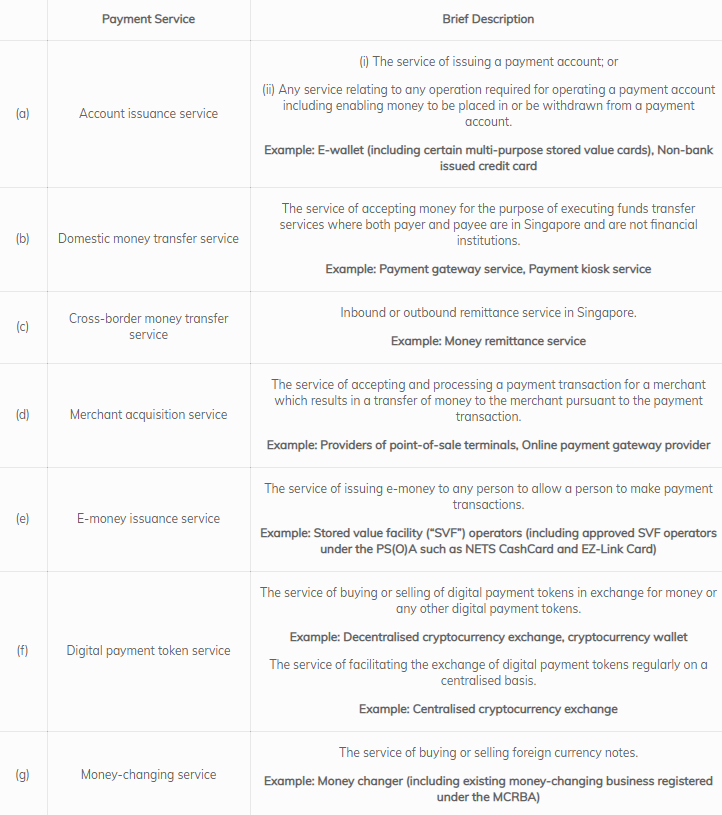

Under the Bill, the following payment services will be regulated:

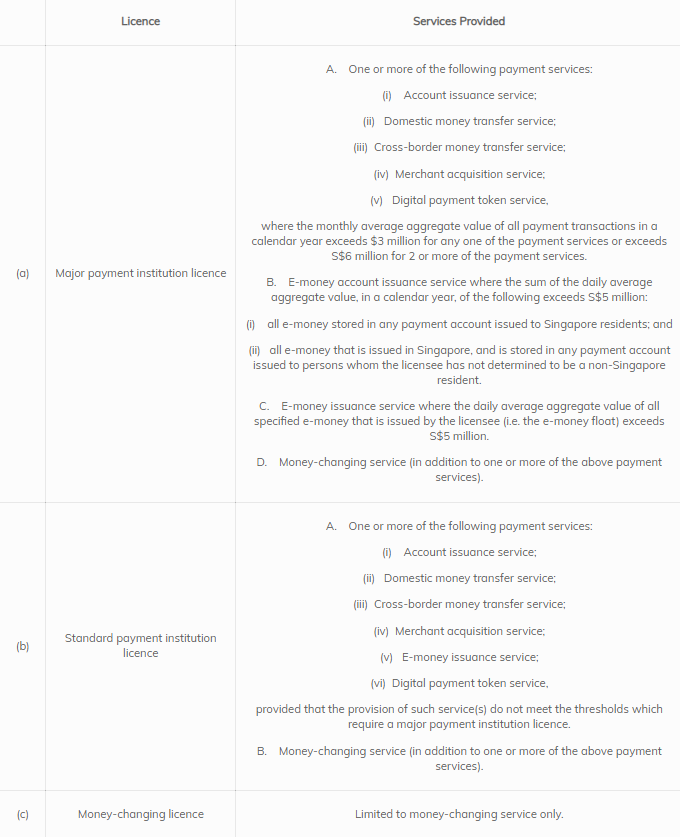

Under the Bill, MAS will adopt a modular approach to licensing payment services, under which payment service providers are not required to obtain a licence individually for each of the payment services they offer, but are required to obtain a licence in one of three classes of licences that corresponds with the level of risk posed by the scale of payment service they provide, namely:

Existing payment service providers who hold:

- a remittance licence under the MCRBA;

- a money-changer’s licence under the MCRBA; and/or

- an approved holder of a stored value facility under the PS(O)A,

will be deemed to have been granted a major payment institution licence that entitles them to carry on a business of providing cross-border money transfer service, money-changing service and/or e-money issuance service respectively.

Regulating Key Risks of Payment Services

The Bill also provides MAS with wide-ranging power to regulate payment service providers and mitigate four key risks applicable to payment service providers identified by MAS, namely:

- money-laundering (“ML”) and terrorism financing (“TF”);

- loss of funds owed to consumers or merchants due to insolvency;

- fragmentation and limitations to interoperability; and

- technology and cyber risks.

The extent of risk mitigating measures which will be imposed on payment service licensees will depend on the specific payment services they provide. Major payment institution licensees may be subject to stricter regulation by MAS, who may:

- direct major payment institution licensees to adopt any common standard, be a participant of a payment system or enter into an arrangement with the operator of a payment system, in order to ensure interoperability between payment accounts and a payment system;

- maintain security of a prescribed amount with MAS for the due performance of their obligations of a major payment institution to its customers;

- safeguard customer monies through an undertaking by any bank in Singapore or prescribed financial institution to be fully liable to the customer for such monies, a guarantee by such bank or prescribed financial institution or depositing such monies in a trust account.

Payment service providers will continue to be subject to the anti-ML and counter-TF obligations imposed by the Corruption, Drug Trafficking and Other Serious Crimes (Confiscation of Benefits) Act (Cap. 65A), the Terrorism (Suppression of Financing) Act and relevant international regulations, and will need to comply with ML/TF risk mitigating measures imposed by MAS from time to time.

The Bill provides transitional arrangements of between 6 and 12 months, allowing payment service providers sufficient time to comply with the regulatory requirements under the Bill. Therefore, in light of the upcoming changes to the regulatory and licensing framework under the Bill, we encourage existing and potential payment service providers to start assessing if the services they provide fall within any of the payment services regulated by MAS under the Bill, and if so, which licence will they be required to obtain.

GENERAL DISCLAIMER

This article is provided to you for general information and should not be relied upon as legal advice. The editor and the contributing authors do not guarantee the accuracy of the contents and expressly disclaim any and all liability to any person in respect of the consequences of anything done or permitted to be done or omitted to be done wholly or partly in reliance upon the whole or any part of the contents.