Date Published: 26 August 2019

Authors and Contributors: Bill Jamieson, Wong Pei-Ling and Marvin Chua.

AMENDMENTS TO THE RULES ON VOLUNTARY DELISTING FROM SGX-ST

The Singapore Exchange Regulation recently announced[1] changes to two key aspects of the voluntary delisting rules to enhance the protection of minority shareholders during voluntary delisting from SGX-ST. These changes, which are effective from 11 July 2019, are summarized below.

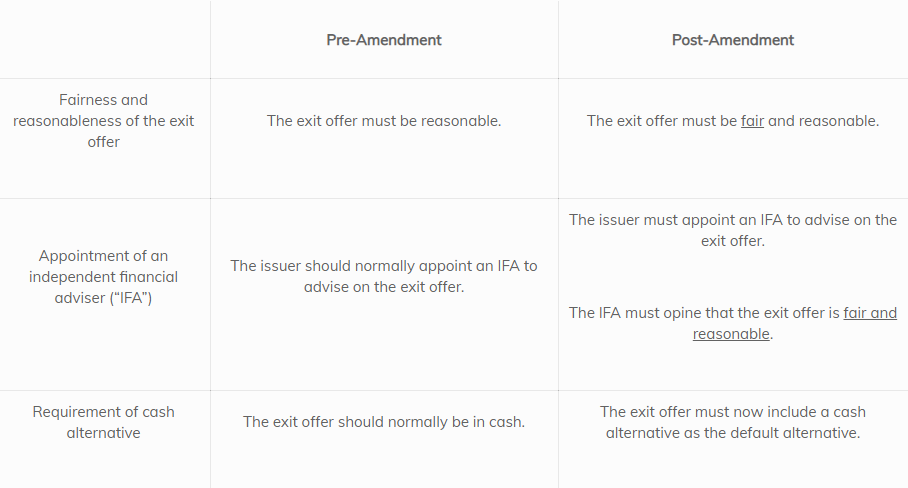

Exit Offer Requirements

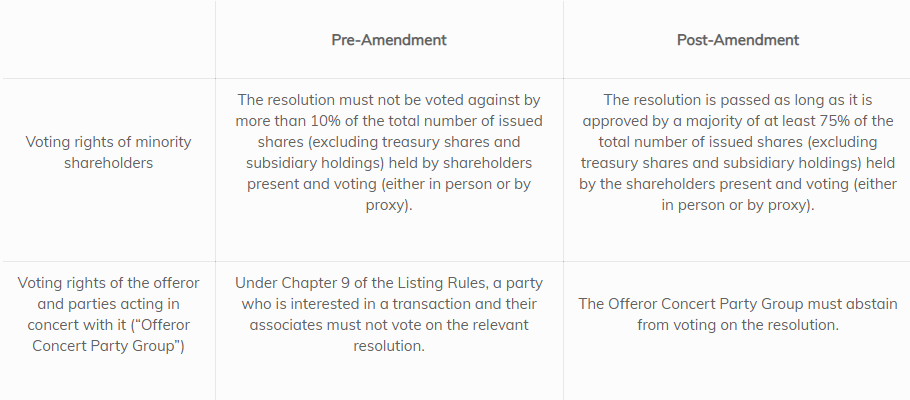

Voting Thresholds for a Voluntary Delisting Resolution

SGX has clarified that the above amendments in respect of the Exit Offer Requirements and Voluntary Thresholds for a Voluntary Delisting Resolution would not apply to:

- a delisting pursuant to a voluntary liquidation; and

- a delisting pursuant to an offer under the Takeover Code provided that the offeror is exercising its right of compulsory acquisition.

In addition, Rule 1307 of the Listing Rules requiring the issuer to obtain the Voluntary Thresholds for a Voluntary Delisting Resolution would not apply to a delisting pursuant to a scheme of arrangement.

Voluntary Delisting (coupled with exit offer) vs Voluntary Offer

In our earlier CNPUpdate article on the privatisation of a company listed in Singapore, we discussed common avenues in which a company listed on the SGX-ST may be privatised. These avenues include a voluntary delisting proposal, coupled with a voluntary exit offer to acquire all the shares of the company (“Exit Offer”) other than those already owned by the offeror (“Offeror”) and parties acting in concert with it (“Offeror Concert Party Group”) and a stand-alone voluntary offer to acquire all the shares of the company other than those already held by the Offeror (“Voluntary Offer”).

Prior to the amendments to the voluntary delisting rules, if a resolution for voluntary delisting was to be voted against by shareholders holding at least 10% of the total number of issued shares of the company, it would not have been possible for an Offeror to privatise a company via the voluntary delisting avenue. Instead, an Offeror may stand a better chance of taking the company private by making a Voluntary Offer.

With the removal of the 10% block under the new voluntary delisting rules however, it may now be somewhat easier for an Offeror to take a listed company private via a voluntary delisting exercise (as the Offeror will need instead to obtain the approval of shareholders (outside the Offeror Concert Party Group) holding 75% of the issued shares present and voting at an EGM of the company). However, the offer has to be fair and reasonable and the Offeror must have the cooperation of the board of the company to convene an EGM of its shareholders.

Conclusion

The changes should be welcomed by independent (and minority) shareholders, as public listed companies are now required to give shareholders a better exit value (which includes a cash component) and the resolution to delist an issuer must be passed by shareholders forming the majority of at least 75% in value present and voting (excluding the Offeror Concert Party Group). The exclusion of the Offeror Concert Party Group from the voting process is also in line with practices in other jurisdictions such as Hong Kong and Australia.

The Board of an offeree company must obtain competent independent advice on the merits of any offer and the substance of such advice must be made known to its shareholders. While previously, an offer only has to be reasonable (and may not necessarily be fair to the minority shareholders, and the independent directors may accept such an opinion), an offer will now have to be both fair and reasonable. By comparison, there is no requirement under the Takeover Code that the offer must be fair and reasonable (unless it involves a disposal of the offeree’s assets to a shareholder).

Following the above amendments to the voluntary delisting rules, SGX will be developing guidance and standards for IFAs and their opinions. We will provide an updated article on the guidelines once they have been issued, which may:

- require the IFAs to separately set out their bases for determining fairness and reasonableness of the exit offer;

- clarify that an exit offer is generally fair if the offer price is equal to, or greater than, the value of the shares which are subject to the offer; and

provide a suggested list of factors to be considered when determining if an exit offer is reasonable, which may include (i) the existing voting rights in the offeree company held by the offeror and parties acting in concert with it and (ii) the market liquidity of the relevant securities.

GENERAL DISCLAIMER

This article is provided to you for general information and should not be relied upon as legal advice. The editor and the contributing authors do not guarantee the accuracy of the contents and expressly disclaim any and all liability to any person in respect of the consequences of anything done or permitted to be done or omitted to be done wholly or partly in reliance upon the whole or any part of the contents.

Footnotes

[1] “SGX RegCo requires exit offers to be fair and reasonable, shareholder vote to exclude offeror and concert parties” (11 July 2019) website: https://www2.sgx.com/media-centre/20190711-sgx-regco-requires-exit-offers-be-fair-and-reasonable-shareholder-vote.